Never Neglect The Metric of Yield on Cost

This metric is the most important, yet most neglected by most investors.

People work hard. They save whatever's left after the bills are paid. Some put the surplus into a cookie jar, content to see cash build up each week.

More sophisticated folks want to see a better return, higher than 0% on their hard-earned money. A certain percentage of those are content depositing their funds at their local bank for a .2% return. Others, seeking better returns than that often deposit funds into a longer term CD and get current returns close to 5.0% today.

Yet another cohort of savers/investors invests its money in stocks that pay dividends to their shareholders. Essentially, this is a bet that as a company earns more money, they'll have more to share with their stakeholders down the road. In other words, the hope is that those dividends will grow higher and higher throughout the years of ownership.

The Search

The search for dividend growers begins in the research an investor can do on any number of financial websites. Yahoo Finance, in particular, is a good resource as it usually sports historical information going back to when a company first initiated the payment of dividends to public shareholders.

Once you find a stock that evidences a long-standing proclivity to not only pay dividends, but to increase them on a steady, annual basis, and has done so for at least ten years, it's time to apply this formula:

CAGR

How Do You Calculate Compound Annual Growth Rate (CAGR)?

The compound annual growth rate (CAGR) shows the rate of return of an investment over a period of time. It’s expressed in annual percentage terms and can be calculated by hand or by using Microsoft Excel.

The easiest way to think of the CAGR is to recognize that the value of something may change over a number of years, hopefully for the better but often at an uneven rate. The CAGR provides one rate that defines the return for the entire measurement period.

You may be presented with year-end prices for a stock like this:

2021: $100

2022: $120

2023: $125

The price appreciated by 20% ($100 to $120) from year-end 2021 to year-end 2022, then by 4.17% ($120 to $125) from year-end 2022 to year-end 2023. These growth rates are different on a year-over-year basis, but we can use a formula to find a single growth rate for the time period.

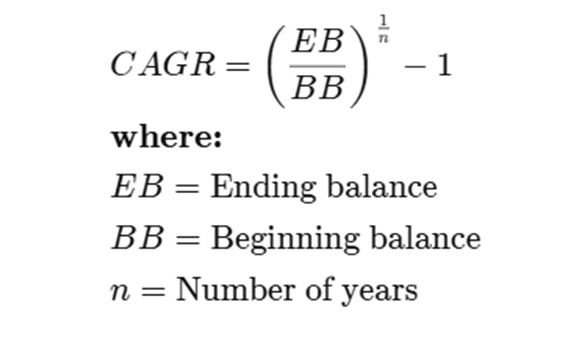

The CAGR requires three inputs: an investment’s beginning value, its ending value, and the time period expressed in years. Online tools, including Investopedia’s CAGR calculator, will give the CAGR when entering these three values. The formula is:

CAGR=(EBBB)1n−1where:EB=Ending balanceBB=Beginning balancen=Number of yearsCAGR=(BBEB)n1−1where:EB=Ending balanceBB=Beginning balancen=Number of years

Plugging in the above values, we get [(125 / 100)^(1/2) - 1] for a CAGR of 11.8%. Its overall growth rate can be defined as 11.8% despite the fact that the stock’s price increased at different rates each year.

Use it to determine the cumulated annual growth rate of the dividend. If the result is one you consider sufficient to outpace inflation and preserve your purchasing power you know you're onto something.

The Look Back

Here's the part that most investors neglect, to the detriment of their potential return on investment. Dividend Income investors, more than anything, are laser-focused on the income their investment generates for them. In order to examine whether your company is performing the way you expected, and whether you should continue holding it, yield on cost must be measured.

What is Yield on Cost?

Let's start first with current yield. If a $50 stock is currently paying a $2.50 annual dividend, the current yield is considered to be 5.0%.

$2.50/ $50.00= 5.0% current yield

As you can see, current yield is simply an expression of what amount a company pays you yearly, divided by the current stock price. This is then expressed as a percentage. In this example it is 5.0%.

What is Yield on Cost, Again?

Yield on cost, on the other hand, is an expression of today's current dividend divided by what YOU paid for your stock.

While this may appear similar, it is actually yet a horse of a different color. To illustrate, let's suppose you bought a company like Realty Income (O), a real estate investment trust that calls itself the “Monthly Dividend Company”. Why the nickname? It's pretty straight-forward, really. While most dividend paying stocks pay quarterly dividends, Realty Income been paying a dividend, monthly, to investors for over 38 years.

Not just any old dividend. This company actually increases the dividend every few months. Fractions of a penny more sometimes. And over those past 38 years, the dividend has increased on an annual basis, without fail, year after year. This is the type of company a dividend income investor looks to as the Holy Grail.

It collects rent from a diversified universe of tenants, including the retail and commercial sectors. And all of the leases it makes have automatic rent escalators built in. That means that inflation is dealt with and overcome in a forthright manner, always brining more cash to the company to invest in more rental properties to increase revenues and earnings on a regular basis. It’s a very virtuous cycle.

This model enables the company to pass on those increases to investors in the form of rising monthly and annual dividends.

Now, back to that all-important yield on cost test. Say you bought Realty Income shares near the lows during the 2008 financial crisis. Overall, stock prices fell around 57%. Some stocks, heavily dependent on interest rates which determine borrowing cost, fell even further. This included sectors like real estate investment trusts of which Realty Income was one.

Had you bought shares then, in February 2009, you would have paid around $16.18 per share. At that time, the annual dividend was $1.65 per/share, making the current yield more than 10%. Since the company, throughout its history as a public company has paid a dividend that yields around 5.0%, I refer to that 2009 yield as an accidentally high yield, twice as high as its historical average. Because they continued to pay the dividend at the same rate while the price collapsed, the resulting 10% high yield is considered accidental, simply due to a compressed price.

Had you held your shares for 16 years, to date, the annual dividend you'd receive is now $2.86 per year.

Since you paid just $16.18 per share, your yield on cost would be. 17.70%.

$2.86/ $16.18 = 17.70. %

As you can see, yield on cost is an expression of today's current dividend divided by what YOU paid for your stock.

The cherry on top here lies in the more than 175% capital gain you'd also have achieved on your investment.

Yield on cost is a mathematical way to determine if your original thesis to invest in a company was correct, after all. The higher the yield on cost, the more dramatically the company has demonstrated what you sought; to share in an ever-growing share of the pie that your company cooked up for you.

On the other hand, if the yield on cost is small and disappointing, or even nonexistent, then this would be a pretty decisive signal to dispose of your shares and move on to greener pastures.

Conclusion

As we near the end of another calendar year, it's always a good time to take stock of your investments. To paraphrase Shakespeare, ’To hold or not to hold’, that is the question. Answer that question correctly with the use of proper metrics and you'll have a very merry Christmas, indeed!

My Real Time Portfolio Trackers and stock market investment applications to enhance your investing returns and income are available here.

Stock Market Investing Applications

To date, subscribers to my investment newsletter, “Retirement: One Dividend at a Time” who faithfully mirrored our portfolio have attained annual dividend income over $132,000.00.

You are welcome to a free, two-week trial to my investment newsletter, “Retirement: One Dividend at a Time”. Just shoot me an email and request your free trial, at geoschneider1@gmail.com

To receive notice whenever I publish new articles, simply click the follow button at the top of the article next to my name. Better yet, also click the “Subscribe” button and you’ll receive an email notifying you whenever I publish. Thank you.

So glad you can join me here today. Please consider becoming a paid subscriber of my Substack community for the full experience and so we can do even more.

The first 10 annual paid subscribers this week will receive the RODAT Portfolio Income Tracker ($99.99 retail value) which will reveal every RODAT stock in our subscriber portfolio, share counts and dividend amounts. With this digital tool, you may track the portfolio and mirror your own portfolio with the names you find suitable for your needs.

In addition, the first 10 annual paid subscribers this week will receive the digital Stock Market Investing Tool of your choice ($99.99 retail value), many of which are in real time and will greatly enhance your potential for capital gain and dividend income.

Make your complimentary choice here.

Retirement: One Dividend at a Time is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

For just $5 per month, or $50 annually, you’ll receive full access to every article I write, complete access to my entire archive of articles, access to a special chat group of similarly minded investors and deep-dive articles for paid subscribers only, with recommended dividend growth stocks to supplement your Social Security benefit.

If you found value in this article and would like to support my efforts, please consider buying me a coffee, here.

buymeacoffee.com/georgeschneider

Discover my archive of articles on Substack, here.

Retirement: One Dividend at a Time is a reader-supported publication. To get the full experience, exclusive chat group, in-depth analysis, receive new posts and support my work, consider becoming a free or paid subscriber.

Other articles readers have found valuable and actionable reading:

Investing in Realty Income: A Smart Choice for Monthly Dividends

This Perpetual Money Well Never Runs Dry

Five Ways to Identify the Most Reliable Dividend Stocks

Potential Recession? Load Up on This Defensive Stock for an 11.5% Yield

Best,

George Schneider

Founder and publisher

Retirement: One Dividend At A Time

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals, and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

Disclosure: I am long all RODAT Portfolio names. The Portfolio continues to build dividend income with reliable, dependable equities which have long histories of increasing the dividend.

Copyright ©2024, George Schneider