How to Pay Only What YOU Want to Pay for Stocks

Selling puts is an easy, conservative way to generate income. Reduce the cost of stock shares to the price you want to pay.

source: Created by author with Microsoft Copilot

What Could Happen If You Sell 6 Puts on Realty Income (O)?

Let’s say you sold 6 put options on a company called Realty Income (stock symbol “O”). You picked a strike price of $55, and the options expire on July 18, 2025. You received $1.10 for each share as a premium. Since each option covers 100 shares, you made $660 total (6 x 100 x $1.10).

Now let’s talk about what might happen next. There are three big possibilities — and we’ll keep it simple.

Scenario #1. The Stock Stays ABOVE $55 by July 18, 2025

Let’s imagine that when July 18 arrives, the price of Realty Income’s stock is more than $55. It could be $56, $60, or even $100 — it doesn’t matter, as long as it’s more than $55.

If that happens, you win!

Nobody will make you buy the stock at $55 because they could sell it for more on the open market. That means your put options expire worthless, and you get to keep all the money you made selling them: That $660 in premiums is yours to keep, and you don’t have to do anything else.

This is the best-case scenario for you.

Scenario #2. The Stock Drops BELOW $55 by July 18, 2025

Now let’s imagine the stock price falls to something like $50 or $45 when the option expires.

If that happens, you’ll be forced to buy the stock at $55 per share, because that’s what the put option contract says.

Since you sold 6 puts, and each covers 100 shares, that means you’ll have to buy 600 shares of Realty Income at $55 each. That’s $33,000 you need to have ready!

But wait — what if the stock is only worth $50 at that time?

Then you’re paying $55 for something only worth $50. That means you’re losing $5 per share, or $3,000 total. But remember — you got paid $660 when you sold the puts, so your real loss is $2,340 ($3,000 — $660). You can see how collecting premiums by selling puts acts as a sort of insurance policy or safety bumper guards on your investment.

If the stock falls more — to $40 or lower — your losses grow. But they’re not unlimited. The worst that can happen is the stock goes to $0 (which is very rare), and you’d lose the full $33,000 minus your $660 premium.

Scenario #3. We’re Happy to OWN Realty Income at $53.90

As dividend income investors, we look for ways to buy shares of companies we want to own at cheaper prices than currently available on the marketplace. Selling puts and collecting premiums is one of those ways. In this instance, buying shares for a net price of $53.90 ($55 cost minus $1.10 premium) allows us to accumulate shares at the price WE WANT TO PAY. Doing so gets us that fat, juicy dividend of 6.0% that Realty Income pays on a monthly basis and has grown on a regular basis for over 30 years.

Put Selling Outcome Table

What to Remember:

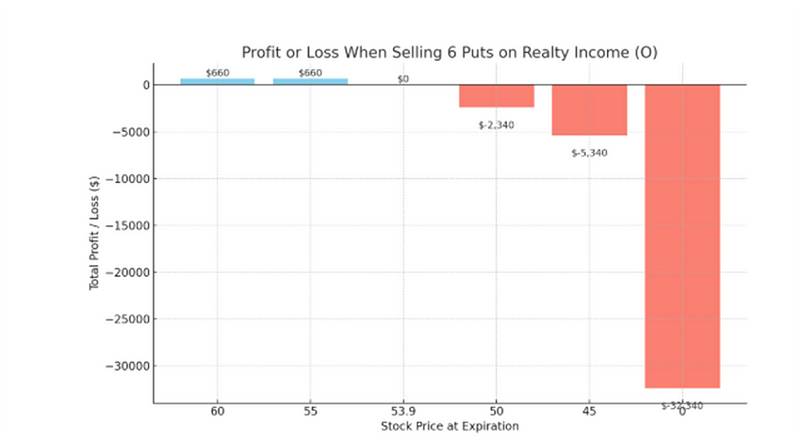

Max gain: $660 (if the stock stays at or above $55)

Break-even price: $53.90

Max loss: $32,340 (if stock goes to $0, but only if you keep your stock till it dies)

You need $33,000 in buying power to cover the purchase if assigned

Here’s a bar chart showing the profit or loss for each possible stock price at expiration. Blue bars mean you make money, and red bars mean you lose money. The taller the bar, the bigger the result — good or bad.

Conclusion

If Realty Income stays above $55, you keep $660, and nothing else happens. Great outcome!

If Realty Income falls below $55, you’ll have to buy 600 shares for $55 each, even if they’re worth less. You lose money if the stock is worth less than $53.90 ($55 — $1.10).

This loss, however, is only a paper loss and only become a real loss if you sell it below $53.90.

Since our main goal is to own Realty Income for less than it is selling on the open market, getting if for a net cost of $53.90 and a 6.0% dividend yield is a win-win in our book.

To do this trade safely, you need to have enough money saved up in case you need to buy the stock.

Selling puts can make you money, but you need to be ready for the risks. Just like a superhero wears armor, you need to have cash protection in case things go wrong, and those cash premiums help do that for you.

Retirement: One Dividend at a Time is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Subscribers to the Retirement: One Dividend At A Time investment newsletter who mirror the RODAT Portfolio have annual income in excess of $138,000.00 from dividends alone.

I don’t have investors or work for a large corporation. My work is fueled by people like you. If you enjoyed this article, would you consider supporting me?

Learn more about me here.

Other articles of mine with over 90,000 views each that readers found worthwhile reading:

Best,

George Schneider, M.A.

Founder and publisher

Retirement: One Dividend At A Time

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals, and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

Disclosure: I am long all RODAT Portfolio names. The Portfolio continues to build dividend income with reliable, dependable equities which have long histories of increasing the dividend.

Copyright ©2025, George Schneider