REITs To Avoid In 2025, part 1

Real Estate Investment Trusts can be great passive investment vehicles. However, not all REITs are the same and some should be avoided.

Not all REITs are worth buying.

Not all REITs are the same.

Some property sectors are risky and overpriced.

Here’s a REIT to avoid in 2025.

The REIT market is vast and versatile with over 1,000 REITs worldwide, and not all of them are equally attractive.

They invest in 30+ countries and 20+ different property sectors and some are facing significant headwinds, all while others enjoy rapidly growing rents. Moreover, there are also vast differences in valuations from one sector to another.

In this article, I am going to highlight one type of REITs that I would avoid investing in this year.

Office REITs

Increasingly, many value investors claim that office REITs are offering a great investment opportunity.

They still trade at a significant discount to pre-covid levels, even as more and more companies are requesting their employees to return to the office.

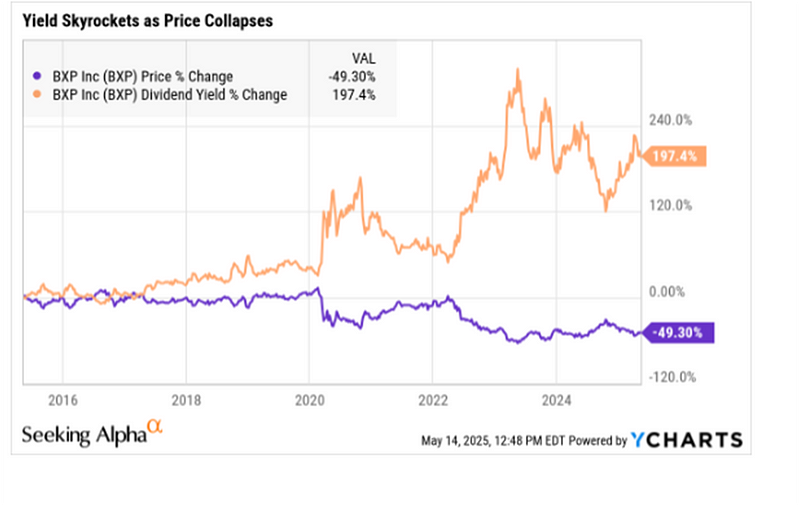

Taking the example of BXP, Inc. (BXP), it still trades at a 49% discount to its 2020 levels and that’s despite all the inflation that we have experienced in recent years, which has increased the replacement cost of its properties.

Notice from this next chart how the dividend yield on this stock has skyrocketed as the price, inversely, has collapsed.

It’s 5% yield, currently $3.92 has seen no increase since 2019. This is not the definition of a dividend growth stock. It is moribund and may take years until it can resume growth in the dividend, if ever. Even though the yield is in the low range, because the company may cut the dividend in the future, it may be regarded by some as a yield trap.

It’s been 10 long years now, and still the dividend has barely budged, from $3.85 in 2015 to $3.92 today.

That’s the bull thesis, if you can call it that, in a nutshell.

But there are significant flaws to it. The main flaw is that even if most companies require employees to return to the office, it won’t change the fact that office landlords will still face significant headwinds going forward.

Most companies have now moved to a hybrid model with their employees working 1–3 days each week from home, resulting in less demand for office space and also different needs.

As a result, vacancy rates have kept shooting higher even as companies returned to the office. Today’s vacancy rates are the highest ever recorded.

Moreover, it is forecasted that the vacancy rates will keep rising closer to 25% in the coming years as older multi-year leases expire.

This means that a lot of office buildings are sitting vacant and landlords are desperate to fill them up, willing to offer significant tenant improvement packages and rent cuts to secure a tenant. Lower rents translate to lower revenue, lower AFFO (adjusted funds from operations) and possibly dividend cuts or eliminations in the future.

I also predict that a lot of these vacant buildings will change hands over the coming years, and as new owners come in, they will heavily reinvest in the properties to make them more competitive with Class A properties. This will then increase the competition and put more pressure even on the best assets.

Another problem is that the needs of tenants have also changed and, as a result, landlords will likely need to heavily reinvest in their properties to keep their tenants happy. If not, they will likely move elsewhere when the lease expires. After all, they have a lot of options in today’s market.

BXP

With that in mind, office REITs really aren’t that cheap.

If you adjust for the capex that will need to be reinvested in these properties just to keep them desirable, then today’s valuation multiples are actually quite high.

For this reason, I have no interest in most office REITs right now.

Retirement: One Dividend at a Time is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Subscribers to the Retirement: One Dividend At A Time investment newsletter who mirror the RODAT Portfolio have annual income in excess of $138,000.00 from dividends alone.

I don’t have investors or work for a large corporation. My work is fueled by people like you. If you enjoyed this article, would you consider supporting me?

Substack is my main writing platform where I publish deep-dive analytical articles that just might help save your retirement. I’d love to have your support here!

Other articles of mine with over 80,000 views each that readers found worthwhile reading:

Best,

George Schneider, M.A.

Founder and publisher

Retirement: One Dividend At A Time

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals, and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

Disclosure: I am long all RODAT Portfolio names. The Portfolio continues to build dividend income with reliable, dependable equities which have long histories of increasing the dividend.

Copyright ©2025, George Schneider

George, I agree with your analysis. MPW appears too risky at this point due to the factors you mentioned. They missed estimates just 17 days ago in revenue and earnings. In addition, they've slashed the dividend in half, twice, within the last 2 years. Not a pretty picture from my angle.

Agree. In that vein - your thoughts on MPW? Some on Seeking Alpha keep seeing it as primed for a turnaround, but I find myself wondering what % of income for its tenants might come from Medicaid patients - the numbers of which will shrink should the BBB get passed in its current form.