Why Accept 3.5% From this Bank When the Dividend Pays 7.0%

Why Accept 3.5% From this Bank When the Dividend Pays 7.0%

Easily double your passive income with a bit of risk.

source: image created by author in Bing

Easily double your passive income with a bit of risk.

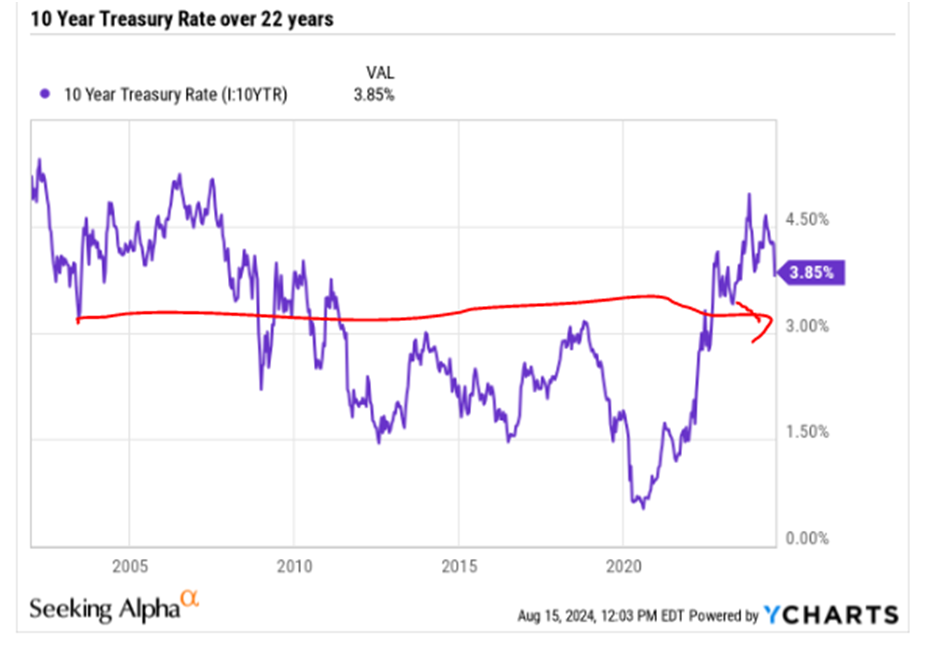

Savers and investors have excellent choices today to grow passive income. At least, compared to several years ago when interest rates went to zero or less. We refer to that era as ZIRP, or zero interest rate policy. But today, the difference an investor can get from a bank’s dividend and the same bank’s savings account interest can be stark.

Particularly when we stand on the precipice of a cut in the Fed’s interest rate in the next couple of weeks, this calculation becomes much more important and meaningful to the investor’s pocketbook.

Investors have put the odds of a rate cut from the Fed at the September FOMC meeting at 75%. And the bet that rates could be cut by ½% has risen to near 50% as of this writing.

This chasm can be so wide that it screams for your attention and consideration.

Why the Difference Between Rates?

1. Savings bank interest is guaranteed by the FDIC in the U.S. and by the Canadian Deposit Insurance Corporation (CDIC) in Canada, backed by the full faith of the Canadian government, up to certain maximums.

2. The dividend is never guaranteed. It is based on the board’s quarterly or monthly determination as to whether the bank’s earnings and free cash flow can safely cover the dividend without jeopardizing the bank’s financial condition and income statement.

3. When a guarantee is offered, savers trade assurances on their capital for a lower income.

4. When no guarantee exists on the dividend, investors must be offered a higher income amount in order to take on the risk that the dividend could be reduced or even eliminated at some time in the future.

How We Determine Dividend Sustainability

· If free cash flow comfortably covers the current dividend, we assign a high degree of probability that the dividend can be sustained or even raised in the future.

· If the p/e of the bank is the same or lower than its peers in the industry, we determine that the stock is being offered at fair value and has room to run in its price.

· When the dividend yield is below its 5 year average, a bargain is being offered along with much higher yield.

· Where the dividend yield is in the general ball park of its industry peers, we judge the dividend to be safe.

· In instances where the dividend yield is much higher than peers, we seek to determine if this is due to temporary factors and that problems will soon be resolved, resulting in an increase in stock price and a reversion to the mean of industry peers as to the dividend yield.

Canadian Banks Differentiated Themselves from U.S. Banks

During the 2008-2009 financial crisis, U.S. banks that had invested heavily in CMS and CMOS obligations suffered badly as many of these securities cratered in value. Canadian banks never exposed themselves to these assets in the way that U.S. banks did. The financial industry has always regarded the Canadian banking industry as much more conservative in its approach to making money.

They still operate in a vanilla-like fashion. They lend out depositors’ money at a higher interest rate than paid to their depositors and make the difference between those yields.

A Canadian Bank That Checks All the Boxes

The Bank of Nova Scotia (BNS) has been on our watchlist for some time to accumulate additional shares in our RODAT Subscriber Portfolio.

We have determined that should the share price fall to $44.00, the $3.07 annual dividend will provide an accidentally high yield of 7.0%. This compares very favorably to the 3.5% interest rate the bank offers on its regular savings accounts. In fact, it will provide double the income per year. Once the saver transitions to an investor and determines this is a pretty safe bet, she will be rewarded with twice the income.

Description

The Bank of Nova Scotia provides various banking products and services in Canada, the United States, Mexico, Peru, Chile, Colombia, the Caribbean and Central America, and internationally. It operates through Canadian Banking, International Banking, Global Wealth Management, and Global Banking and Markets segments. The company offers financial advice and solutions, and banking products, including debit and credit cards, chequing and saving accounts, investments, mortgages, loans, and insurance to individuals; and retail automotive financing solutions. It also provides business banking solutions comprising lending, deposit, cash management, and trade finance solutions to small, medium, and large businesses. In addition, it provides wealth management advice and solutions, including online brokerage, mobile investment, full-service brokerage, trust, private banking, and private investment counsel services; and retail mutual funds, exchange traded funds, liquid alternatives, and institutional funds. The Bank of Nova Scotia was founded in 1832 and is headquartered in Toronto, Canada.

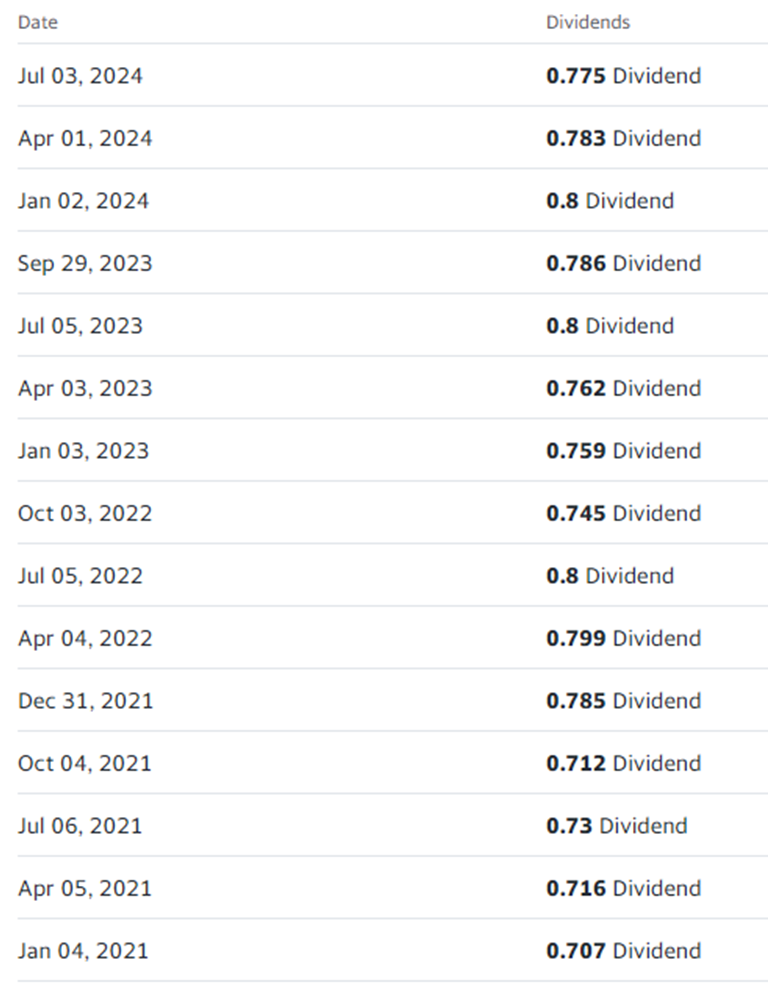

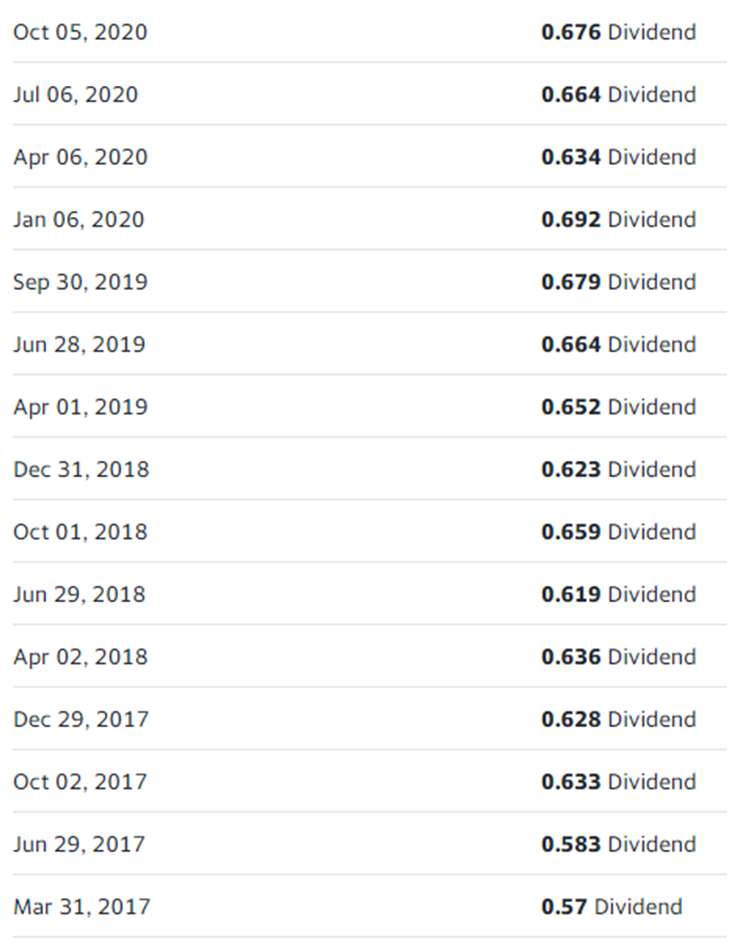

Dividend History

Seeing is Believing

A quick perusal of the dividend history shown above reveals that in 22 years of paying a dividend, the company only slightly reduced the dividend, by about 12%, in the 2009 financial crisis for just two quarters. After that, the company continued in its winning ways, steadily and consistently increasing the dividend. Over a period of 22 years, BNS has more than quadrupled the dividend paid to investors, handily overcoming inflation by a huge margin.

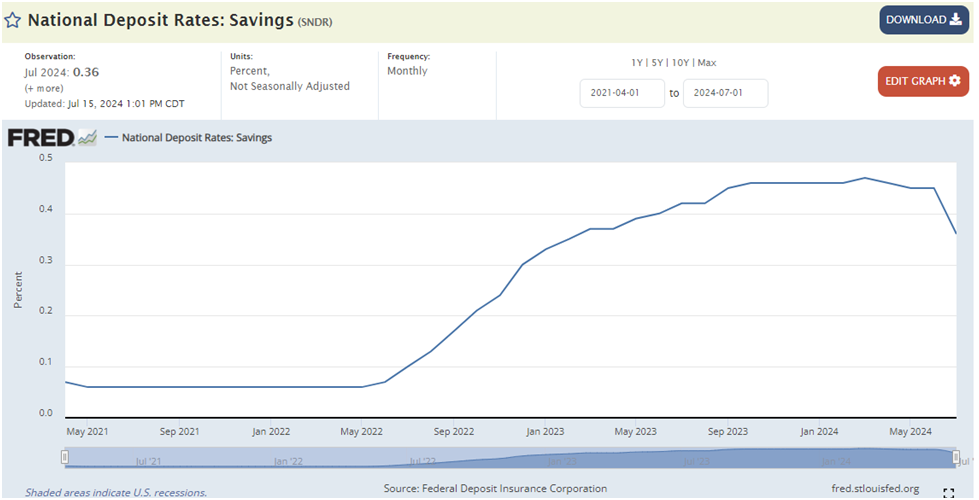

Over the same time period, interest rates paid to depositors on their savings accounts stagnated for most of this time as the Federal Reserve pressured rates lower as part of their liquidity program to help banks and corporations thrive and allow consumers and businesses to borrow cheaply.

This is what banks, on average, paid out to their savings bank depositors over the past three years.

You can see that the average savings bank interest rate rose 9X, from about .05% to about .45% before dropping recently to about .35%.

Recent Catalysts That Pressured the Stock Price

In recent years, the payout ratio, what percent of earnings the bank pays in dividends, has risen from less than 48% to more than 71%. Investors are more comfortable when the payout ratio is lower. Their comfort level is tested when it rises above its historical record or that of its industry peers.

For investors looking for a bargain, this is one indictor to keep in mind.

Earnings from Continuing Operations

Another recent catalyst that lowered the stock price is the company’s earnings from continuing operations. Some investors will shy away from a company that is reporting a declining trend in this regard.

However, with the prospect of a lower Federal Funds rate coming in the next several weeks, this new catalyst alone should lend support to the thesis that earnings will reverse to the upside in coming quarters.

Higher earnings will lend sustainability to the dividend.

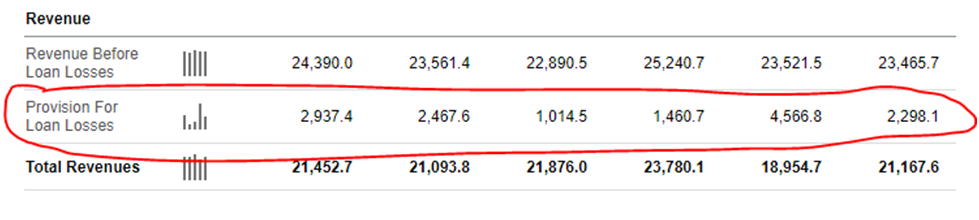

Provisions for Loan Losses

This metric has been in a steady uptrend for the last few years. It is the opposite of what investors are looking for. Increasing the provision for loan losses means the bank has identified loans that are underperforming or bound to be so in the near future. They are therefore required by regulation to set aside large amounts in very safe, low yielding investments in the event those loans becoming non-performing. This, necessarily, lowers the amount a bank can earn on its deposits with the bank.

Again, with the fast-approaching end of the low interest rate environment, the Fed is signaling that the economy is strong,, the labor market continues to be strong and inflation is coming down ( the August 15th report from the Fed that inflation has fallen below 3.0% for the first time since 2021). With these factors coming into clear sight, non-performing loans should decrease and the bank should be able to reduce provisions for non-performing loans. This will enable the bank to free up capital to earn higher amounts on its re-deployed capital.

Bottom Line

When we are able to identify companies whose stock prices have fallen only temporarily due to several near-term catalysts, and believe other near-term catalysts will begin to support the stock price and pressure it higher, we set our target prices for stock accumulation. In this instance, Bank of Nova Scotia checks the boxes and represents clear value and accidentally high dividend yield and income.

So glad you can be here today. Please consider becoming a paid subscriber of this community so we can do even more.

By becoming a paid subscriber to my newsletter you will enable greater volumes of work with higher levels of investment news with deeper analysis and content to come your way.

Just hit that Subscribe button below and get my new articles directly in your inbox.

If you’d like a free, two-week trial of our investment newsletter, “Retirement: One Dividend at a Time”, specializing in dividend growth investing, just shoot me an email and ask, at geoschneider@hotmail.com

Best,

George Schneider, M.A.

Founder and publisher

Retirement: One Dividend At A Time

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals, and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

Disclosure: I am long all RODAT Portfolio names. The Portfolio continues to build dividend income with reliable, dependable equities which have long histories of increasing the dividend.

Copyright ©2024, George Schneider

Thanks for reading Retirement: One Dividend at a Time! If you found value, please consider upgrading to paid to receive new posts and support my work.